Baby Step 3b Even if in a House Already

Dave Ramsey's 7 Baby Steps could be the answer to all your financial problems. But it's not all sunshine & roses. Find out if it's for you!

I can't believe it, I've done it again! You sit and think, I'm up to my eyeballs in bills and suffocating from the pressure and stress that comes when another bill arrives. I've been here before, and I've dug my way out of debt, and I can do it again!

But you wonder, will this time be any different? Or will you find yourself back in the same spot in five years? You're not sure, and you don't want to think about it. But this time, it has to be different! How do you make sure this never happens again?

Don't worry; the answer is simple, it's the baby steps by Dave Ramsey. Now the answer is simple, but it won't be easy. It will be hard, but Dave and the millions that have executed Dave Ramsey's baby steps will be right there beside you.

This time, with the 7 Baby Steps Program, you will dig yourself out of debt, change how you think about money, and will live like no one else! Are you ready? Good!

This post may contain affiliate links. If you make a purchase, I may make a commission at no cost to you. Please read my full disclosure for more info

Who is Dave Ramsey?

Dave Ramsey is considered America's money coach. The guy that will give it to you straight, no BS and no sugar coating it. You don't want to hear what he has to say because it won't be pretty. But trust me, it's precisely what you need to change your financial life!

In his early 20's he had millions by flipping houses. He was invincible, so he said, then one day it all came crashing down. He was dead broke, with a wife and two kids and no hope. But somehow, he turned it all around by changing how he handled his money and how he thought about it. He started to read the bible and followed God and grandma's ways of handling money. He then taught tens of thousands how to dig themselves out of debt and change their finances forever.

Long story short, he's sold over 11 million copies of his seven times bestsellers, has a radio show that 13 million people hear, and has a net worth, according to Investopedia, to be over $200 million in 2021. That's quite a life and makes him qualified to teach you about personal finance.

What are the 7 Baby Steps?

Dave Ramsey's method for changing your financial life starts with his baby step program. You follow along with his financial plan and do what he says to do in the order he's outlined. You don't skip steps! He's helped over 5 million people go through Financial Peace University, his course for teaching the baby steps program. But don't worry, you don't need to do the full class, you can go through it on your own. There's lots of support with Facebook groups, resources like books, podcasts, and DVDs to help you along the way.

Let's take a quick look at what the 7 Baby Steps are…

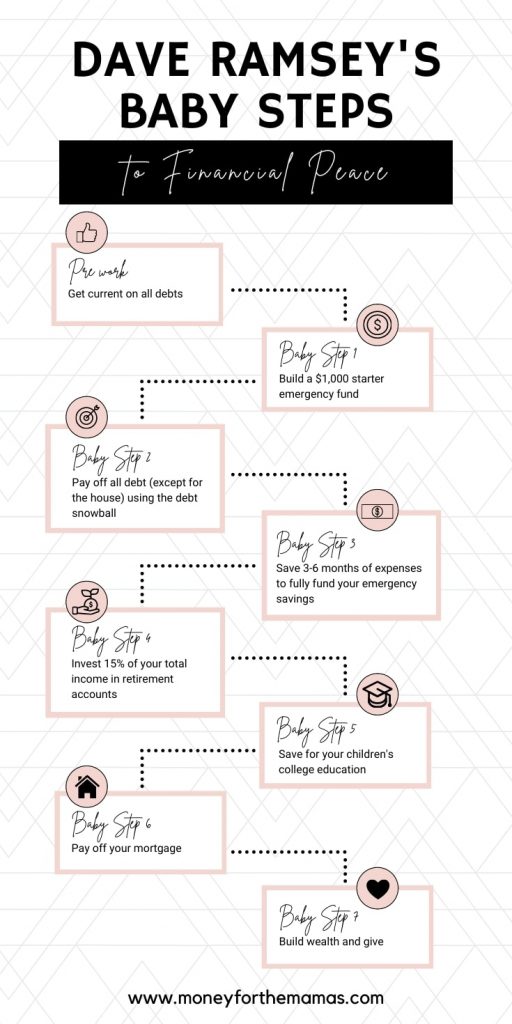

The 7 Baby Steps

- Save $1,000 starter emergency fund

- Pay off all debt (except your house) using the debt snowball method

- Save 3-6 months of living expenses in your emergency fund

- Invest 15% of your household income in tax-advantaged retirement accounts

- Save for your kid's college education

- Pay off your home early

- Build wealth and give.

He talks all about the baby steps in all of his books, but it wasThe Total Money Makeover that launched his method into the stratosphere of success! In that book, he states, "The way to eat an elephant is one bite at a time. Find something to do and do that with vigor until it's complete; then and only then do you move to the next step. If you try to do everything at once, you will fail."

He continues that "the power of focus is what causes the baby steps to work." It's a strategic plan that focuses on human behavior to win the war on debt.

Easy Savings & Free Money

- Sign up with ibotta and get $5 cash back on your first purchase!

- Earn points on ANY receipt from ANY store and redeem for gift cards with the fetch rewards app.

- Earn cash back from over 4,000 retailers with TopCashback when you buy online. Even on gift cards, at restaurants, and hotels.

- Join Rakuten and shop at your favorite stores for up to 40% cashback; use the link and get a $10 Welcome Bonus!

- Sign up with Inbox Dollars and get paid to read emails, watch videos, and take surveys. Easy peasy!

- Save money at the grocery store with Coupons.com on things you already buy! This isn't cash back; it's instant savings at the register!

- Get free gift cards & cash for the everyday things you do online at Swagbucks. Use the link and get a $10 bonus

- Save money on gas by signing up with GetUpside; it gives you up to .25 cents cash back per gallon! Use the link when you sign up; you'll get a .15 cents per gallon bonus!

Baby Step 1 – build a starter emergency fund

Vote: Good

It's important to note that you need to be current with your creditors before you can begin step one in Dave Ramsey's plan.

Everyone has heard the saying "save for a rainy day," but what does that even mean? Well, bad things will happen, and when I say bad, that means expensive things that you must buy/pay for. For example, your car breaks down; you need emergency surgery, a giant sinkhole opens up in your driveway.

You need to be able to pay for these emergencies with cash! Many people get confused. Why not pay off debt right now? Well, if you haven't saved anything, and an emergency happens, you'll have to put it on a credit card. Then you'll be right back to square one, which can be a huge mental setback.

Consider saving $1,000 to be a mental cushion, sort of a warm-up exercise for what you need to later one. A huge sense of pride and accomplishment comes from saving that amount if you never have done it before. Remember, winning with money is a mental and behavioral game!

When you save your rainy-day fund, define what constitutes an "emergency" in your household. As very few things are actual emergencies. We tend to call things an emergency when we haven't planned appropriately.

For example, buying new tires for your car isn't an emergency. That should be a planned purchase, as you should have known that you would need new tires someday. (Hint: I set up sinking funds for these types of expenses, they are a lifesaver!)

Dave often talks about doing things fast; he calls it gazelle speed. He wants you to do things fast by throwing everything you have into the process. This way, you keep motivation high and see quicker results.

To do this step, the first thing you'll need to do is to get a household budget together. I know people dread this step, but it's honestly not bad at all. It's more of a mental game than anything. So know that a budget is planning where you want your money to go. The good news is that there are lots of ways to budget.

If you are all in on the Baby Steps plan, you can do the Dave Ramsey budget, or if you want some more options be sure to check out the 7 Proven Budgeting Methods. You can also do your budget on Dave Ramsey's EveryDollar app! It's simple, straightforward, and free! Here's what you have to know about the EveryDollar budget app.

Get your $1,000 starter emergency fund together and stick it somewhere safe where you won't be tempted to borrow it. One of the best things that Dave's seen is a lady sent him a picture of her beginner emergency fund. She framed 10 $100 bills in glass and wrote "in case of emergency break glass" with a dry erase marker on it. Yes, you can get at it, but if you've taken that much effort to save it and frame it, you will most likely do everything possible not to break that glass!

Baby Step 2 – pay off all consumer debt (except for the house with the debt snowball method

Vote: Good

Debt freedom is the ultimate financial goal for so many Americans, so a lot of the Dave Ramsey plan is built upon this stepping stone. Here is the baby step that you need to pay particular attention to doing this "the right way." There is a strategy in play, and it's very important. The debt snowball is a debt payoff strategy, as well as the debt avalanche, and the last option is throwing money haphazardly at your debts and hope for the best.

- Debt avalanche method –is where you put all available extra money at paying off the debt with the highest interest rate.

- Debt snowball method – is where you put all available extra money at paying off the smallest debt balance first, and then once that's done, move on to the next smallest balance.

The debt avalanche will save you the most money over the entire process, but your likelihood of finishing the plan is a lot lower than with the debt snowball method. The snowball method focuses on getting the quickest wins by paying off small balances because it keeps you motivated! Again, paying off credit card debt is a psychological and behavioral process.

Yes, you continue to pay all the minimum payments on your debts, but not a penny extra. Put everything towards the smallest balance. As the name implies, as a snowball rolls down the hill, it picks up more snow and goes faster and faster, just like your debt payoff journey.

For example, let's save you have $378 a month to put towards your debts, debts of…

- Credit card 1: $3,677 with 24% interest, a minimum payment of $73

- Credit card 2: $876 with 27% interest, a minimum payment of $17

- Personal loan of $5,000 with 14% interest, a minimum payment of $100

With the debt snowball, you'd pay #2, then #1, then #3. It would take you only five months to pay off your first debt and be completely debt-free in 2.5 years!

Dave Ramsey's Baby Step 3 – save 3-6 months of expenses

Vote: Good

Remember that starter emergency fund back in step 1? Well, now that you have cleared your debt, you can throw a lot of money into building a fully funded emergency fund. Dave recommends 3-6 months of living expenses kept in a separate & safe bank account. (Safe from you borrowing it).

For example, I hold our emergency fund in a high yield savings account in Ally bank. It is entirely separate from our checking and other savings accounts, which we use as sinking funds.

Why do you need 3-6 months of living expenses set aside? If you get seriously injured and can't work, or your spouse gets really sick, and you have to be home to take care of the kids while they're in the hospital, or if a global pandemic hits and you get laid off, and no one is hiring. Hey, it could happen.

Right now, it's August 2021, and in the past 18 months, I never heard one person say, "Geeze, I had too much in savings." So far, everyone wished that they had a fully-funded emergency savings account.

A full emergency fund is security; it's peace of mind knowing that you can still feed your family with a roof over your head and the electricity running. And let me tell you, peace of mind is a hard feeling to beat!

Now, if you want, have a 9-month emergency fund or a full one year of expenses set aside. But you shouldn't go too much over that as you could be losing a lot of growth if you invested that money. Remember, your emergency fund isn't supposed to make you money; it's supposed to bring you security.

The size of your emergency fund should also be determined by your family size, your employability, and the debts you have.

A single person needs a lot less than a mom with three children. If your town's job market has high unemployment, then have a higher emergency fund, as it may take you longer to find a job. If your family has frequent medical needs, then absolutely have a larger emergency fund. Customize it according to your situation but never go lower than three months of living expenses and don't go higher than one year.

As Dave puts it, an emergency fund can turn a crisis into an inconvenience.

Baby Step 3b

What? There are sub-steps? Yup, every good plan sometimes needs to be tweaked, so Dave introduced baby step 3b.

3b is when you rent while working the baby steps, but would like to own a home. So 3b is saving for your home. Dave would, of course, like everyone to pay cash for their home, but in today's housing market, that isn't very realistic.

Dave begrudgingly admits that you may need to take on debt to purchase a home. So 3b is saving for that downpayment, ideally at least 20% of the cost, so you don't pay private mortgage insurance (PMI).

Yet, even better is if you only take on a 15-year fixed-rate mortgage. That's his bottom line. So you may be in this step for two years or so. But in the long run, you will save SO MUCH in interest; it is well worth it!

Dave Ramsey's Baby Step 4 – invest 15% of your income in a retirement account

Vote: Very Good

With baby steps 1-3b, you should do those on their own, one after the other. When you get to baby step 4, you can do that in line with baby steps 5 -7.

Baby step 4 is where you focus on long-term wealth building, with financial independence being the goal! Retirement savings is exciting! Well, I think it's exciting as I love earning compound interest! Remember, Albert Einstein famously said …

"Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn't… pays it."

And when Einstein says something, your ears better perk up!

So, according to baby step 4, you need to invest 15% of your gross household income in a retirement account, ideally, tax-advantaged accounts. That means in a workplace 401k or an IRA (Roth is advised, but you can do a traditional IRA).

Note: don't count your social security benefits as part of your 15%; this is entirely separate.

Dave recommends that you invest in growth stock mutual funds to build wealth. Which is fine; he can say anything he wants. On the other hand, I am not a CFP, so I'll just tell you what Dave says.

The number one complaint that people voice against Dave Ramsey is that his stated rates of returns on his mutual funds are grossly overestimated. Dave says you can get 12% returns. According to the balance, "Since 1926, the average annual stock market return has been roughly 10%." Which is a lot less than 12% (yes, even 2% makes a drastic difference. Yet, you also have to consider inflation, which brings the returns down to 7%, which most people quote as an average rate of return on the stock market.

So here's the plan of attack…

- If your employer offers a match, contribute just enough to get the full match amount. So if they contribute 4%, you contribute 4%. That match amount is free money; never leave it on the table!

- Then take the remainder of your 15%, so in this example, 11% remains and invest it into a Roth IRA.

- Roth IRA – you contribute money (that has already been taxed), and it grows tax-free over the years.

- Traditional – you contribute before-tax money (your gross amount), and then when you withdraw it in 40 years, you pay taxes on it.

Which should you choose? That's a debate as heated as what came first: the chicken or the egg. It all depends on your current tax bracket and what you think your tax bracket will be when you need to withdraw the funds.

Why not invest everything into your employer's retirement plan? Well, you could, but usually, these funds have a lot fewer investment options than what you should choose from with your own IRA. If your company has lame investments with high fees (anything over 1%), then go out and open your own IRA.

You will most likely need your own IRA anyways, as when you change jobs you'll want to roll over those funds to a place where you can control it.

All of his books talk about The Baby Steps, yet we've focused on The Total Money Makeover for this post. Yet, once you reach baby step 4, you are encouraged to start looking ahead. Dave's book,The Legacy Journey, details the considerations you should be planning for in the next 10-20 years. You can find a review of that book, along with all his other books, right here.

Baby Step 5 – save for your children's college fund

Vote: good

Baby Step 5 is the most debated baby step. Should you pay for your kid's college? Well, yes and no. But let's talk about Dave's perspective.

Dave feels that a college education is a foundational step. Kids, if they want to, should go to college and get a degree. BUT, Dave isn't too picky about the college; he prefers in-state, public colleges. Because honestly, unless you went to an Ivy League college, no one cares where you graduated from. Only a few professions benefit from an Ivy Leagues education. So save your money; it's off to a state college for Jr.

Opening a college fund usually means opening an ESA or a 529 account. Where the contributions grow and can be withdrawn tax-free when used for specific educational purposes. Each state has its own plan, and you aren't tied to your state's plan; you can choose any state's program. Check out Saving for College to get the best info on 529 plans and your other options.

An important note – start college funding as early as possible as growth from compound interest will be key! So, by all means, begin when your kiddos are babies if you're able to.

Don't forget, have your child apply for all the available scholarships and grants; this can be very lucrative! And as a parent, contribute what you can afford, and then take out student loans for the gap.

As many so wisely put it, kids can take out loans for college. You cannot take out a loan for retirement! So don't shortchange yourself to cover your child in this instance.

According to Nerd Wallet, the average student loan debt for a bachelor's degree among the class of 2019 was $28,950. Yikes! Specifically, these were the average costs of colleges for the 2020-2021 academic year:

- Public four-year in-state: $26,820.

- Public four-year out-of-state: $43,280.

- Private nonprofit four-year: $54,880.

That's a hefty amount of debt to chain a college graduate to. Paying it off will take time and dedication. How long, you ask? Well Saving for College estimates, "most loan holders typically take no more than 16-19 years to pay back their federal student loans." yes, there is a federal standard repayment plan of 10 years. But it's not so cut & dry.

I would so much rather put a small amount of money into an account every month than crush my child with the weight of student loan debt that would take her 20 years to pay off. But that's my personal opinion.

Dave Ramsey's Baby Step 6 – pay off your mortgage

Many people also argue with Dave's reasoning (and math) when it comes to his advice to completely pay off your home.

Yes, with a mortgage payment, you get a tax deduction, and you could have invested that money and got lucky with a high rate of return. But again, it's hard to argue with the feeling of owning your own home 100%. No one can take that away from you! Remember, having debt means an increase in risk. Total peace of mind comes from having zero risk. That means paying off your home.

This chapter of The Total Money Makeover gives a few examples of tax credits, interest rates, and potential returns, but I won't bore you with those numbers. As the point remains, when you own something, it's yours, and you are a slave to no lender; you are the master!

Baby step 7 – build wealth

Vote: The ugly

Baby Step 7 is the last step. You've worked hard, and now it's time to enjoy the fruits of your labor. Dave states that "I can only find three good uses for money. Money is good for FUN. Money is good to INVEST. And money is good to GIVE." And when you reach this baby step, you can do all three of those things! That's the mindset of financial freedom!

Dave always recommends tithing 10% of your income, and then you can always give more if you want. Now, for my own opinion. There's a lot to be said for helping others, but for it to be a true gift, it needs to be your choice. Money given out of guilt or obligation will only make you resentful, which is the exact opposite of how you should feel when you wholeheartedly give. So this part of the Baby Steps gets "the ugly" vote.

Almost all of us can find a cause that we believe in. For my family, we donate to Give Kids the World, a nonprofit that provides critically ill children and their families a magical vacation in Orlando, Florida. Yup, they help kiddos go to Disney World and meet Mickey or their favorite Disney Princess.

Now you don't need to donate to a nonprofit; you can give in many ways. You can give money to a friend's Go Fund Me account if they fall on hard times. You can donate to your church that's helping a local family buy Christmas presents. You can donate your time, skills, and labor to any cause of your choosing. Whatever you do, do it with your whole heart.

Dave also wants you to have fun with your money. If you've worked the plan, and have all your bases covered, then, by all means, have fun! Go on vacation! Buy a nicer car, eat at fancy restaurants! If you can afford it, you should enjoy it!

To continue having fun with your money, you need to invest some of it, so you can keep earning and withdrawing funds. If you are at this step, a CFP can help you with proper withdrawal rates, tax planning, etc.

Baby Step 7b – the pinnacle point

Reaching this baby step essentially means that you can coast, go ahead and put your feet up; your money is working all on its own! This is when your investments make enough to support you and your family. You are retired and financially secure.

According to Dave, you've reached this point when you can live off 8% of your portfolio. Congrats, you've "made it!"

The Bad

Dave Ramsey is a huge fan of using cash or debit, he despises credit cards. With good reason, he got into trouble overusing his credit cards. Firstly, it's brave to admit your weaknesses and/or faults. I applaud him for knowing himself.

Yet, you shouldn't paint everyone with the same brush. People are different and so are their downfalls and skills.

For others, using credit cards responsibly can be part of a good saving strategy. Many people use credit cards (called churning) to gain a lot of financial benefits through reward programs. I myself, use a 2.5% cashback credit card for everything I buy. You better believe that I pay the bill off in full every month, and I have a plan for those reward points! If you don't pay off your bill the interest accrued completely negates any reward points gained.

At the end of the day

If you've come this far in this post, you have conquered the most challenging part, believing that a different and better financial life could be yours. Seriously, that's the hardest part. Stating your journey towards financial peace is simple; if you follow Dave Ramsey's baby steps, but that doesn't mean it will be easy. In fact, it will be hard. But so is being in debt.

Being broke is hard, getting out of debt is hard. Choose your hard.

Dave Ramsey

Articles related to the Baby Steps by Dave Ramsey:

- Your Complete Guide to Choosing the Best Dave Ramsey Book for You

- How to Use Dave Ramsey's Budget Percentages to Make Your Perfect Budget

- The Dave Ramsey How to Budget for Financial Peace Guide

- Here's What You Have to Know About the EveryDollar Budget App

What do you think of Dave Ramsey's Baby Steps? Are you ready to change your life once and for all?

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.Accept Read More

Baby Step 3b Even if in a House Already

Source: https://www.moneyforthemamas.com/baby-steps-by-dave-ramsey/

Belum ada Komentar untuk "Baby Step 3b Even if in a House Already"

Posting Komentar